AWS has increased prices for reserved AI GPU capacity by around 20%, highlighting the growing shortage of high bandwidth memory and advanced chips. As demand outpaces supply, AI development costs are rising, making large scale model training and deployment more expensive.

Anthropic’s reported 1.4 GW Australian AI tender signals a major investment opportunity, but also a harder sovereignty question: will Australia and the Global South build capability inside this frontier infrastructure, or remain dependent on foreign chips, models, permissions and inference margins?

At midyear, the AI race has become a contest for global power. Energy, chips, cybersecurity, capital markets and state intervention now shape who controls the inference economy, who pays for it, and who is left exposed in the next industrial order of machines, markets and sovereignty to come ahead.

Nvidia’s blockbuster quarter, Cerebras’ vertiginous IPO and Huawei’s state backed ascent reveal both the promise and fragility of the emerging inference economy, where capital, chips and geopolitics now move in lockstep across Washington, Wall Street and Beijing.

The fragile boom at the heart of the inference economy

Nvidia’s latest earnings, Cerebras’ vertiginous IPO and Huawei’s state backed ascent are now read as markers of a historic industrial buildout. They are also warning lights on a much more fragile system. Industry observers are broadly optimistic about the “inference economy” that is forming, yet they increasingly describe a contested future in which capital whiplashes between favourites, geopolitics hardens around silicon, and the downside of overreach grows with every upgraded forecast.

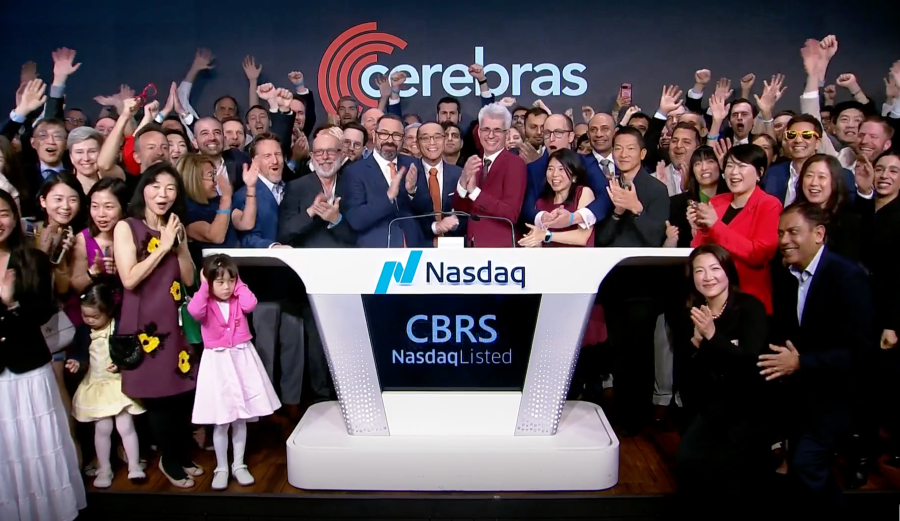

Image Credits: Nasdaq

This week’s Nvidia story starts with the numbers but does not end there. The company’s first‑quarter results again beat expectations, with strong data centre revenue and guidance that CNBC said “reassured a nervous market that AI demand is not slowing yet,” even if the stock reaction was more restrained than during earlier phases of the boom.

Speaking to CNBC after the release, Jensen Huang acknowledged the volatility in Nvidia’s share price but argued that “concerns around the company have been clearly addressed” by the consistency of AI infrastructure demand and the breadth of customer commitments, from hyperscalers to emerging model labs such as Anthropic. He framed the quarter less as a one‑off win and more as another proof point that Nvidia is becoming the operating system for a new class of AI‑enabled businesses.

That message was amplified on stage at Dell Technologies World just days earlier. There, Huang joined Michael Dell to unveil a refreshed Dell AI Factory with Nvidia, anchored on the new Vera Rubin NVL72 rack that, according to Nvidia, can deliver up to 10 times lower cost per token than its own Blackwell platform for massive‑scale agentic AI inference.

“Now we have, for the very first time, useful AI,” Huang told the audience, explaining that the industry has moved “from generative AI as content to agentic AI as doer,” with agents planning, reasoning and executing workflows rather than merely producing text or images. He and Dell talked up early evidence that such systems can compress tasks like software development from “a month to a week.”

Nvidia CEO Jensen Huang and Dell CEO Michael Dell discuss agentic AI, the demand for memory and the outlook for the China market Source: Bloomberg

Wall Street has largely endorsed that view, albeit with caveats. Morgan Stanley estimates that nearly 3 trillion US dollars of AI related infrastructure investment will flow through the global economy by 2028, with about 2.9 trillion US dollars in data centre construction costs alone, and suggests AI will contribute roughly a quarter of US GDP growth this year. JPMorgan Asset Management, for its part, argues that “business integration of AI is likely to be characterised by stops and starts” and warns that infrastructure bottlenecks, rising costs and uneven adoption will demand “disciplined management” rather than blind faith.

In practice, the market is doing both at once. Schwab Network and others note that Nvidia’s earnings beat has met a “muted” reaction in the stock, as investors weigh fierce optimism against already stretched valuations. Yet those same investors are willing to ascribe eye watering value to newer stories that promise participation in the same buildout.

Cerebras, humanoids and a contested peace

Cerebras’ listing is the most striking recent example. The IPO priced at 185 US dollars after the range was repeatedly raised, opened at 350 US dollars, and closed day one at 311.07 US dollars, delivering what CNBC called a “blockbuster debut” that briefly pushed the company towards a mid 60‑billion dollar valuation. A day later the stock slid around 10 per cent as traders took profits, underlining both the appetite and the volatility that now define AI infrastructure trades. The underlying pitch is serious: a wafer scale chip that promises faster, cheaper inference at scale and a multiyear partnership with OpenAI that Cerebras and its backers describe as “the largest high speed AI inference deployment in the world.”

Analysts see this as both an alternative and a complement to Nvidia. One Wall Street commentator summarised the mood by saying Nvidia’s latest report was “another pop the champagne moment” but adding that “there will be other winners in the AI race,” with Cerebras now firmly in that conversation.

The question is whether capital can keep rewarding companies with constant, stellar percentage growth when they are already worth tens of billions of dollars, and whether that expectation is remotely sustainable across an entire ecosystem. As a marker of where the market is today, Nvidia closed at 219.51, down -1.77% on Thursday’s Nasdaq session, while Cerebras ended at $281.86, down 3.04%, still implying a multi‑tens‑of‑billion‑dollar valuation for a newly listed challenger.

Forward looking research only raises the stakes. Goldman Sachs now projects that the global humanoid robot market alone could reach around 38 billion US dollars within the next decade, while McKinsey sees general purpose robotics climbing towards 370 billion US dollars by 2040, with AI chips and orchestration layers capturing most of the value.

At scale, those humanoids, factory robots and autonomous vehicles are effectively “physical AI infrastructure” that will extend the inference economy from server racks into warehouses, hospitals and roads. The same chips and software stacks that power today’s language models will sit inside humanoids and Robo‑taxis, deepening the link between capital markets and everyday life.

That brings the geopolitics into even sharper relief. Huawei, headquartered in Shenzhen, has become the flagship for Beijing’s attempt to build a sovereign AI hardware stack as US export controls squeeze Nvidia’s most advanced shipments. Chinese policy is deliberately steering demand towards domestic accelerators such as Huawei’s Ascend line, while Washington, Brussels and middle powers from Tokyo to Canberra scramble to secure “safe” supply chains and domestic data centre capacity.

Recent diplomatic set pieces, including high profile meetings between President Trump and President Xi Jinping, are billed as efforts to slow the slide into open rivalry and sketch out a minimum level of cooperation on shared infrastructure and technical standards. In that context, Morgan Stanley’s analysts argue that geopolitics is now an active force “reshaping where and how capital is deployed,” pushing governments and investors to prioritise secure, domestic digital infrastructure and tighter control over critical AI bottlenecks. From that vantage point, the Trump–Xi choreography looks less like theatre and more like risk management, an attempt to contain escalation so both sides can keep building their own AI capacity without tipping markets or supply chains into crisis.

JPMorgan takes a more openly sceptical line on how far such stabilisation can go. Its strategists emphasise that the US and China are already pursuing “different approaches to development and monetisation” of AI, and they expect that divergence to deepen as systems move off the screen and into autonomous vehicles, robotics and other forms of physical automation. In their telling, diplomatic summits may buy time and reduce headline risk, but they do not change the underlying incentives: each side still wants to secure the most advanced chips, the most resilient fabs and the densest data centre networks.

Set against Morgan Stanley’s focus on capital reallocating towards “trusted” domestic infrastructure, the JPMorgan view reads as a reminder that even carefully stage‑managed Trump–Xi encounters sit inside a broader structural contest that no amount of photo‑ops can fully smooth away.

That tension goes to the heart of the hegemony question. An inference economy built on abundant, cheap compute ought to support broad based prosperity, yet the structure of competition makes that far from guaranteed. Two superpowers are now pushing the world’s technological frontier, each with an incentive to control as much of the stack as possible, from fabs and foundries to data centres, humanoids and Robo‑cars. Open markets and state capitalism both amplify the stakes, rewarding speed and scale more readily than caution.

The combined signal from Nvidia’s earnings, Cerebras’ trading and Huawei’s quiet consolidation is that the buildout is very real and still in its early innings. The combined risk is that the same forces driving that buildout also deepen fragility, in markets and geopolitics. Whether the next decade delivers a genuinely abundant inference economy or a more brittle, contested one will depend less on the brilliance of the hardware and more on the choices that investors, regulators and governments make while the champagne is still flowing.

Get the stories that matter to you. Subscribe to Cyber News Centre and update your preferences to follow our Daily 4min Cyber Update, Innovative AI Startups, The AI Diplomat series, or the main Cyber News Centre newsletter — featuring in-depth analysis on major cyber incidents, tech breakthroughs, global policy, and AI developments.

Sign up for Cyber News Centre

Where cybersecurity meets innovation, the CNC team delivers AI and tech breakthroughs for our digital future. We analyze incidents, data, and insights to keep you informed, secure, and ahead.

Anthropic’s reported 1.4 GW Australian AI tender signals a major investment opportunity, but also a harder sovereignty question: will Australia and the Global South build capability inside this frontier infrastructure, or remain dependent on foreign chips, models, permissions and inference margins?

At midyear, the AI race has become a contest for global power. Energy, chips, cybersecurity, capital markets and state intervention now shape who controls the inference economy, who pays for it, and who is left exposed in the next industrial order of machines, markets and sovereignty to come ahead.

AI’s memory bottleneck is now reshaping the chip war. Apple’s search for Chinese supply, Micron’s pricing power, South Korea’s expansion and Nvidia’s HBM demand expose a harder truth: the AI boom is becoming a test of cost, sovereignty and global dependence across every device and data centres now.

The AI race has left the lab. Washington can stop a chip at customs and weights at a server, but not a rival learning from a conversation, as Anthropic's Alibaba claim shows. The contest now runs through memory, power and the question of which models stay walled and which spill into the open.

Where cybersecurity meets innovation, the CNC team delivers AI and tech breakthroughs for our digital future. We analyze incidents, data, and insights to keep you informed, secure, and ahead. Sign up for free!