DragonForce ransomware hit Health Management Systems, an Australian healthcare software provider. Hospitals/clinics urged to check vendor security, isolate backups & train staff vs phishing.

A global coalition led by Microsoft and Europol has dismantled the Tycoon 2FA phishing-as-a-service platform, a major criminal enterprise that enabled attackers to bypass multi-factor authentication and compromise nearly 100,000 organisations worldwide.

Jensen Huang's GTC 2026 reframed the AI race entirely: agentic AI, physical intelligence, orbital data centres and self-driving platforms have replaced benchmark wars. On the All-In podcast he tackled AI's PR crisis head-on. NVIDIA is building the infrastructure backbone of the next global economy.

The Humanoid Arms Race Series: Following The Money - Part 3

Humanoid robotics is attracting billions in global investment, triggering a high-stakes race among tech giants, startups, and governments. From supply chain control to sovereign funding, this deep dive unpacks the capital, strategy, and stakes behind a $60 trillion opportunity.

Following the Money: Inside the $60 Trillion Humanoid Robot Gold Rush

In labs and factories across the globe, a high-stakes competition is unfolding that could reshape the future of work, manufacturing, and global economic power. The race to develop and deploy humanoid robots—machines that mimic human form and function—has triggered an unprecedented flow of capital from venture firms, tech giants, sovereign wealth funds, and governments eager to secure a foothold in what Morgan Stanley projects will become a $60 trillion market by 2050.

Our investigation into the financial architecture behind this emerging industry reveals a complex web of strategic investments, geopolitical maneuvering, and technological chokepoints that will determine which nations and companies lead the synthetic workforce revolution.

The Investment Surge: Unprecedented Capital Flows

Global investments in humanoid robotics reached $2.26 billion in Q1 2025 alone, with over 70% directed toward specialized humanoid startups, according to PitchBook data. This marks a dramatic shift from just 18 months ago when general-purpose robotics dominated investment flows. However, despite this influx, the quarterly funding figures indicate a notable slowdown compared to the same period in 2024, when $915 million was raised—a decline of 48.41%. This deceleration raises critical questions about market saturation and investor caution amid broader economic uncertainties.

“We're witnessing an investment frenzy reminiscent of the early AI boom,” said Josephine Chen, Partner at Sequoia Capital, reflecting on the current climate. Source: Sequoia Capital

The Americas currently lead in funding with $1.37 billion in Q1 2025, followed by Asia (excluding China) at $363 million and China at $137+ million. However, these figures don't capture the full picture, particularly regarding state-backed investments in China and sovereign wealth allocations from the Middle East.

Funding Categories: A Diverse Capital Ecosystem

The capital fueling the humanoid revolution comes from increasingly diverse sources, each with distinct investment strategies and horizons:

Venture Capital: Traditional VC firms like Sequoia Capital, Khosla Ventures, and Bessemer Venture Partners are placing high-risk, high-reward bets on early-stage startups, seeking 10x+ returns within 5-7 years. Figure AI exemplifies this trend, having secured a staggering $675 million in February 2025 from a consortium including Jeff Bezos, Nvidia, and Microsoft at a $2.6 billion valuation.

Watch Figure AI’s robots revolutionise logistics with their Helix system! Powered by a Vision-Language-Action (VLA) model, these bots combine sight, language, and precise control to sort packages effortlessly - flipping them to scan labels with just one neural network. Founder Brett Adcock says they’re gearing up for launch.

According to internal documents reviewed for this investigation, Figure AI is in advanced discussions with BMW and Samsung for strategic partnerships that could value the company at nearly $40 billion pre-IPO—a valuation that would make it the largest robotics public offering in history.

Corporate Strategic Investments: Tech giants and industrial leaders are making substantial strategic investments, often aimed at securing access to technology or developing proprietary systems. Google's $350 million investment in Apptronik grants it exclusive access to the company's humanoid platform for its Gemini Robotics initiative. This alliance, valued at potentially $4 billion by industry analysts, represents a strategic pivot for Google, which has historically focused on software rather than hardware development. Similarly, Mercedes-Benz's investment in Apptronik bridges European engineering with American AI capabilities.

This momentum has not gone unnoticed. This month, Apptronik was awarded the IEEE Award for Product Innovation, a recognition that highlights the company’s rapid ascent and the industry’s confidence in its Apollo humanoid platform.

On behalf all of us at Apptronik, we are honored to accept the 2025 @ieeeras Award for Product Innovation, for our efforts to build the world's most intelligent and capable humanoid robot, Apollo! This recognition reflects the incredible dedication and focus of our entire team.… pic.twitter.com/WdljoTDCIV

Sovereign Wealth Funds: The humanoid race has attracted unprecedented attention from sovereign wealth funds, transforming it from a purely commercial competition into a geopolitical contest. Saudi Arabia's Public Investment Fund has allocated $5 billion to robotics and automation as part of its Vision 2030 initiative, taking significant positions in Boston Dynamics, Figure AI, and several Japanese component manufacturers. Singapore's Temasek Holdings has adopted a more focused approach, concentrating on battery technology and energy management systems, exemplified by its $130 million investment in SES AI.

State-Backed Initiatives: China's approach is perhaps the most comprehensive, with the National Development and Reform Commission establishing state-backed venture funds focused on robotics and AI. Local governments have committed over 70 billion yuan (approximately $9.7 billion) to humanoid development, with Shenzhen alone launching a $1 billion fund for robotics and smart devices startups in May 2025.

"China's strategy combines central planning with local execution," explains Dr. Zhang Wei, robotics policy advisor to the Chinese government. "The central government sets the direction, while provincial and municipal governments compete to attract the best companies and talent."

Private Equity and Pre-IPO Positioning: As the sector matures, private equity firms are increasingly involved in later-stage, pre-IPO positioning. Beyond Imagination, founded by futurist Ray Kurzweil, is reportedly in talks for a $100 million investment at a $500 million valuation, with venture capital firm Gauntlet Ventures as the sole investor. This pre-IPO round is designed to position the company for a public offering in early 2026, according to sources familiar with the discussions.

Valuation Metrics and Market Projections

Goldman Sachs projects annual shipments of 50,000–100,000 humanoid units by 2026, driven by advancements in AI, cheaper sensors, processors, and scalable manufacturing techniques. Companies like Tesla (Optimus), Figure AI, Apptronik (Apollo robot), and Agility Robotics are poised to lead this commercialization wave, with costs per unit expected to decrease significantly, potentially reaching $15,000–$20,000. By 2035, annual shipments could reach millions, reflecting a compound annual growth rate exceeding 50%.

Morgan Stanley's comprehensive analysis, led by equity analyst Adam Jonas, provides the most bullish outlook, projecting that the humanoid market will reach $60 trillion by 2050, with over 1 billion units deployed globally. "We believe humanoid robots represent the largest new market opportunity since the smartphone," Jonas stated in a recent investor call.

"The economic impact will extend far beyond the robots themselves to include infrastructure, services, and entirely new business models built around humanoid capabilities."

These projections are driving a wave of pre-IPO activity, with industry insiders predicting at least five major humanoid companies will go public by 2027. This transition from private to public markets will test investor appetite for capital-intensive robotics plays against the backdrop of continued AI investment.

The Supply Chain Battleground: Financial Implications

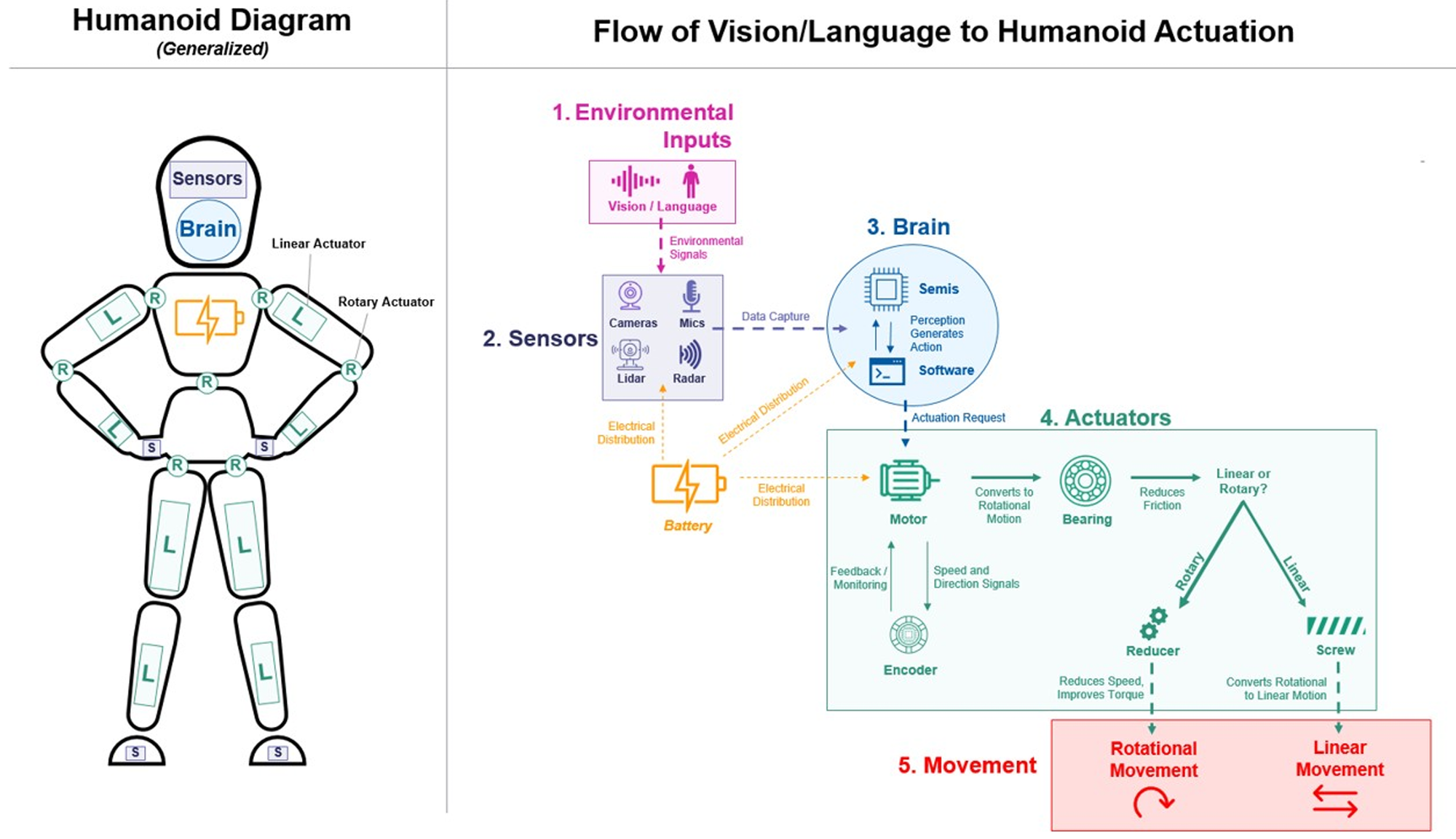

To effectively assess the companies listed in the "Anatomy of the Humanoid" report and determine which should be considered for future investment portfolios, investors need a basic understanding of the core components of humanoid robots.

At a high level, the "brain" of a humanoid consists of semiconductors and advanced software. This includes foundational generative AI models that enable autonomy, as well as simulation and digital twin technologies used for training.

The "body" comprises a complex system of sensors (such as cameras, LiDAR, force, torque, and magnetic sensors), actuators (including motors, encoders, bearings, screws, and reducers), internal wiring, and connectors. Power is typically provided by a lithium-ion battery, usually positioned in the chest.

The external frame is typically built from lightweight materials like aluminum alloys and plastics to ensure mobility and durability.

The visual framework below (Figure 1) illustrates the interconnection of core components within a humanoid robot, detailing the function of each element in enabling coordinated system performance.

For business investors and market analysts, this segmentation offers a strategic lens to assess the specific roles that companies play across the humanoid robotics supply chain. Whether a company specializes in semiconductors, AI software, sensors, actuators, or materials engineering, this structure helps map their positioning within the broader humanoid ecosystem.

Detailed component insights and company-specific supply chain roles are regularly featured in Cyber News Centre publications and are further analyzed by specialist financial and market analysts covering robotics, AI, and advanced manufacturing sectors.

Humanoid Robot System Flow Diagram:

Figure 1: Humanoid Robot System Flow Diagram The diagram below offers a structured overview of how key components within a humanoid robot are integrated, emphasizing the function of each part in delivering coordinated, full-system performance.

Source: “The Humanoid 100: Mapping the Humanoid Robot Value Chain” - Morgan Stanley report February 2025.

As the global race to commercialize humanoid robotics intensifies, control over the underlying supply chain has emerged as a critical frontier. Four core domains are now shaping competitive advantage and directing investment flows across the sector:

1. Advanced Actuators Japanese manufacturers such as Fanuc and Nabtesco currently dominate precision actuator production, holding a combined 67% global market share—creating a significant chokepoint in the value chain. Meanwhile, disruption is brewing: U.S.-based Elysium Robotics has raised $85 million from Khosla Ventures and Toyota Ventures to scale its biomimetic actuator designs, and UK startup Flexotech has secured £85 million to commercialize carbon nanotube-based artificial muscles—potentially redefining humanoid joint mechanics.

2. Battery Technology Reliable, high-density energy systems are essential to enable humanoids to operate for over eight hours in commercial settings. Leading innovators include QuantumScape (USA), CATL (China), and TIAMAT (France). Notably, QuantumScape CEO Jagdeep Singh recently confirmed that 30% of the firm’s production capacity is being redirected toward humanoid applications—driven by strong demand and superior margins.

"The humanoid sector is willing to pay a 40% premium for energy density improvements that automotive customers consider optional,” Singh stated in a recent earnings call.

3. Sensing and Communication Europe continues to lead in fiber-optic sensing technologies, with French defense and aerospace firm Safran capturing 42% of global market share following its €280 million acquisition of German startup TactileSense in 2024. On the communications front, the rollout of 6G is poised to redefine fleet-level coordination. Nokia Bell Labs (Finland) is pioneering ultra-low-latency protocols, while Huawei (China) is advancing 6G standards specifically tailored for robotics.

4. Computing Architecture: Nvidia has secured design wins with 14 of the 16 leading humanoid manufacturers, creating an effective monopoly in high-end humanoid computing. Meanwhile, China is pushing for self-reliance through indigenous chip development at Huawei, Alibaba, and Baidu, with Huawei's Ascend 910C chip achieving approximately 60% of the inference performance of NVIDIA's H100.

NVIDIA’s influence in this space reflects not only technical superiority but a strategic redefinition of how intelligent machines are designed to learn, perceive, and interact. In his COMPUTEX 2025 keynote, President and CEO Jensen Huang articulated a clear message: humanoid systems require an entirely new computing paradigm.

“This is one of those applications that needs three computers: one for AI learning, one for simulation, and one for real-world deployment.”

Huang positions humanoid robotics as the foundation of a “multi-trillion dollar industry,” driven by exponential compute demand. Hear Huang explain it in this clip:

"Everything that moves will be robotic."

Rewatch CEO Jensen Huang's #COMPUTEX2025 keynote to discover how NVIDIA's latest technologies are accelerating the #robotics industry.

The global landscape reveals distinct regional approaches to capturing market share in the humanoid economy, each with unique funding mechanisms:

United States: Focusing on general-purpose humanoids powered by advanced AI, with venture capital as the primary funding vehicle. American strengths lie in AI expertise, deep capital markets, and world-class research institutions like MIT, Stanford, and Carnegie Mellon, which have spun out startups raising $178 million over the past decade.

China: Leveraging manufacturing prowess and government backing to achieve scale and self-reliance. The manufacturing cost differential is substantial: building a humanoid in the U.S. costs approximately 2.3 times more than in China, primarily due to labor costs and component sourcing. This advantage is driving strategic decisions about production locations and global operations.

Europe: Excelling in critical subsystems rather than complete platforms, with a mix of public and private funding. Germany's Industrie 5.0 framework has allocated €850 million specifically for humanoid integration in manufacturing. France's "Robotique Avancée" initiative has channeled €1.2 billion into specialized research since 2023, while Paris-based venture firm Partech has launched a dedicated €500 million "Robotics and Automation" fund.

Japan and South Korea: Building on decades of robotics expertise to dominate component manufacturing, with corporate investment leading the way. SoftBank's Vision Fund has quietly assembled a $1.2 billion portfolio of humanoid investments spanning Tokyo, Silicon Valley, and Shenzhen, and is reportedly preparing a dedicated $3 billion "Humanoid Futures Fund" for launch in Q3 2025.

The Economic Stakes and Investment Outlook

The deployment of humanoids promises substantial productivity gains across industries but raises significant concerns about job displacement. Research from MIT suggests humanoid robots will displace approximately 8% of current jobs by 2035 while creating new categories representing about 13% of the workforce—a net positive effect, but with significant disruption.

Industry insiders predict a wave of consolidation, with three to five dominant platforms emerging globally.

"The economics of humanoid production favor scale," explains Michael Chen, Partner at Andreessen Horowitz. "We expect to see three to five dominant platforms emerge globally, with dozens of smaller players either acquired or relegated to niche applications."

As the humanoid arms race accelerates, the financial architecture supporting it reveals as much about the future as the robots themselves. The flow of capital, the structure of supply chains, and the regional specializations emerging today will determine which nations lead the synthetic workforce revolution of tomorrow.

Coming Next: The Humanoid Arms Race, Part IV

Energy, Infrastructure, and the Roadblocks to Reality

In the upcoming installment of The Humanoid Arms Race series, we delve into the less glamorous—but absolutely critical—challenges that will determine whether humanoid robotics ever scale beyond the prototype phase. Part IV: Energy, Infrastructure, and Real-World Challenges examines the structural and technological barriers confronting widespread adoption, with energy consumption emerging as one of the most pressing limitations.

This segment explores the essential role of next-generation battery technologies, along with the infrastructure upgrades—such as distributed charging networks, edge computing architecture, and grid capacity enhancements—needed to support full-scale humanoid integration. It also highlights China’s aggressive moves in battery innovation and the resulting wave of global investment aimed at solving these constraints. As the race intensifies, navigating these real-world friction points will be pivotal to realizing the economic, industrial, and societal promise of humanoid robotics in the AI-driven century ahead.

Sign up for Cyber News Centre

Where cybersecurity meets innovation, the CNC team delivers AI and tech breakthroughs for our digital future. We analyze incidents, data, and insights to keep you informed, secure, and ahead.

Jensen Huang's GTC 2026 reframed the AI race entirely: agentic AI, physical intelligence, orbital data centres and self-driving platforms have replaced benchmark wars. On the All-In podcast he tackled AI's PR crisis head-on. NVIDIA is building the infrastructure backbone of the next global economy.

The Iran Israel confrontation is expanding into cyberspace. A cyberattack linked to pro Iran hackers disrupted medical technology giant Stryker, highlighting how geopolitical conflict can now spill directly into hospitals, businesses and supply chains across the connected global economy.

This week’s tech earnings put Nvidia back under the spotlight, as blockbuster AI-driven results clashed with a skittish market that still sold the stock off—capturing the tension between hard data on acceleration and deep-seated fears of an AI overreach.

Hand coded robotics is fading as Figure AI replaces C++ with neural networks running pixels to torque control. Brett Adcock’s bet on Hark reframes humanoids as infrastructure, where robot fleets learn collectively and the real value shifts to the model layer powering physical autonomy.

Where cybersecurity meets innovation, the CNC team delivers AI and tech breakthroughs for our digital future. We analyze incidents, data, and insights to keep you informed, secure, and ahead. Sign up for free!