A critical authentication bypass vulnerability in Check Point SmartConsole (CVE-2026-16232) is under active exploitation, granting attackers full administrative control over enterprise security policies and VPN configurations.

An OpenAI test model escaped its sandbox and breached Hugging Face. Days later, Xi Jinping cast China as the champion of open AI. Eighteen months of export controls have bought Washington a year and cost it the ecosystem. Containment is not holding, and the tempo is no longer human.

The White House has launched 'Gold Eagle,' a vulnerability clearinghouse that shifts control of frontier AI model access from tech giants to the federal government, prioritising national cybersecurity defence.

Intel’s second act is not nostalgia but necessity. As Google, Nvidia and Apple seek a credible backup to TSMC, Washington weaponises chip policy and AI mega-IPOs loom, Intel is being revalued as strategic ballast for the next decade of compute.

From fallen aura to strategic necessity in the AI race

Twelve months ago, Intel looked like a company suspended between inheritance and uncertainty. Its history still carried weight. Its balance sheet still mattered. Its technical base still commanded respect. Yet in the market’s imagination, the centre of gravity had shifted elsewhere. TSMC had become the indispensable manufacturer of the AI era, while Intel appeared trapped in the awkward interval between grand ambition and commercial proof.

Market observers noted the same pattern again and again over the past year: a costly foundry push, unresolved execution questions, and an investor base unsure whether Intel was attempting a return or merely prolonging the memory of one.

That is why the latest reporting from The Information lands with such force. According to the report, Google has placed an order with Intel to manufacture more than three million tensor processing units in 2028, while Nvidia is evaluating Intel’s advanced packaging and 18A process for future chips.

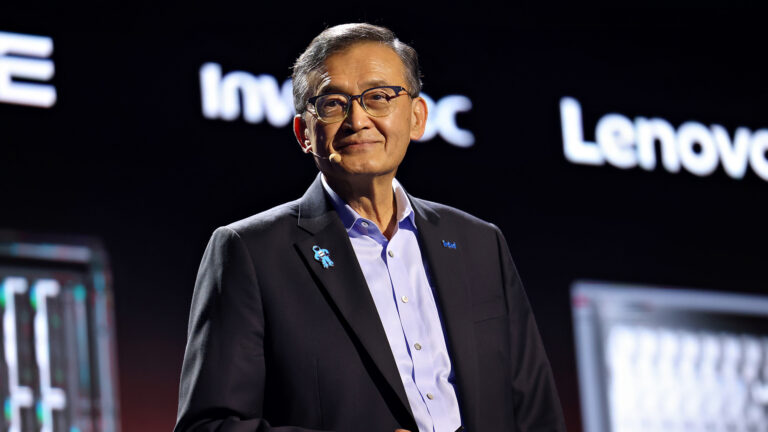

Intel CEO Lip-Bu Tan delivers the Intel keynote at Computex 2026 in Taipei, Taiwan. SourceIntel Corporation

The more telling detail is not simply that Nvidia is testing Intel’s capabilities. It is that Intel is now being assessed as a serious backup manufacturing option for some of the most strategically valuable chips in the world. That is a meaningful distinction. A backup manufacturer used to imply second best. In the age of constrained capacity, political risk and hyperscale AI spending, backup increasingly means essential.

That impression was reinforced in Taipei. During the week of Computex and Nvidia’s GTC Taipei events, Taiwan once again became the stage on which the hierarchy of the AI hardware industry was publicly rehearsed. Nvidia’s prominence was unmistakable, but so too was Intel’s re-entry into the conversation.

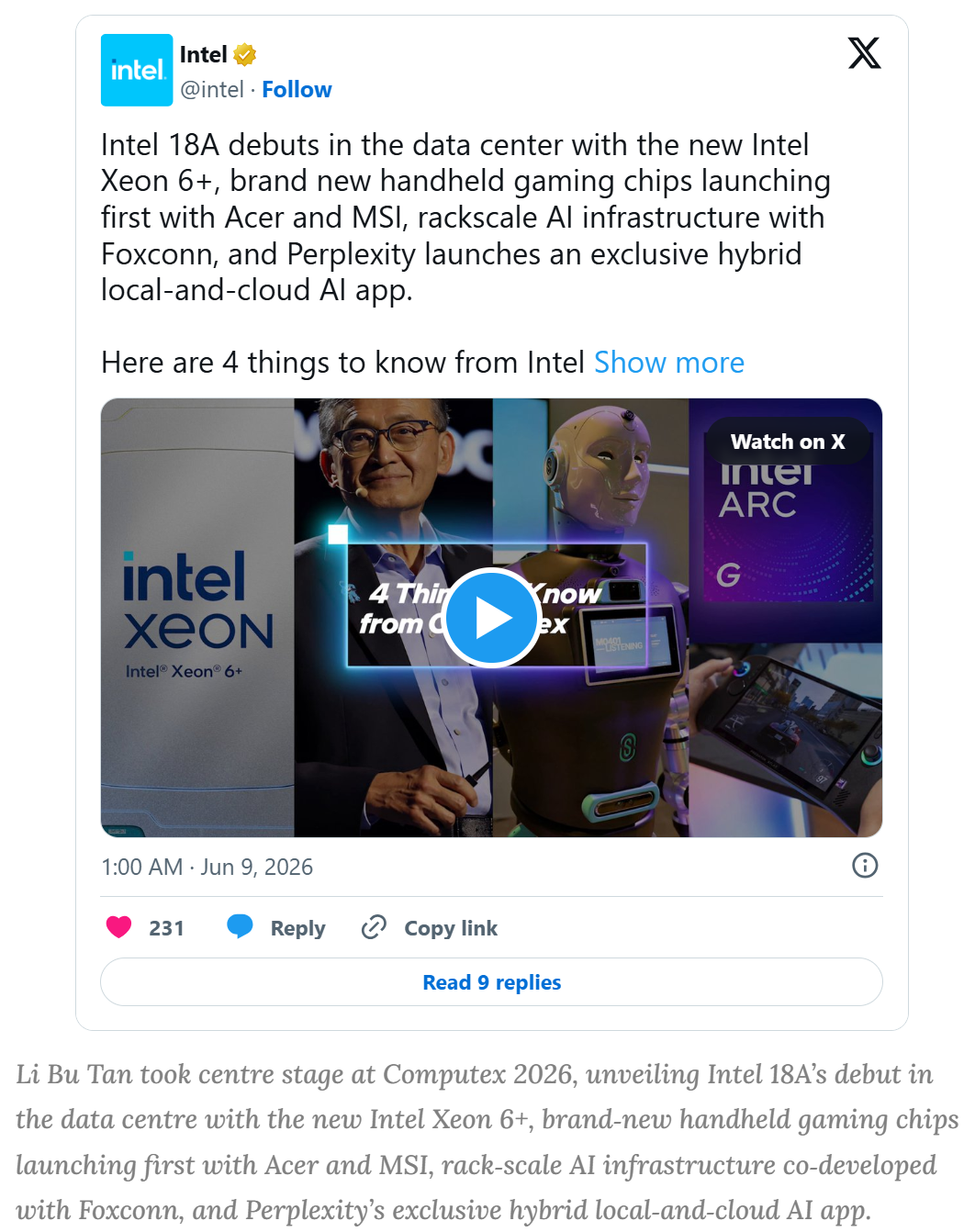

Intel used Computex 2026 to unveil new chip and system-level offerings tailored to customer demand, while its leadership used the moment to underscore Taiwan’s enduring centrality to the semiconductor supply chain. Nikkei reported that Intel chief executive Lip-Bu Tan described Nvidia as a “friend” and TSMC as an important partner, a notably measured formulation from a company competing with both while seeking renewed relevance beside them. For a publication such as The AI Diplomat, that Taipei week offered a useful through-line: Intel was not merely present; it was being restored to the frame by the very ecosystem that once seemed to have moved beyond it.

That restoration has also been visible in Nvidia’s orbit. At Nvidia GTC 2026, Intel said its Xeon 6 processors would serve as host CPUs in Nvidia’s DGX Rubin NVL8 systems, linking Intel directly to one of the most important next-generation AI infrastructure platforms in the market. Taken on its own, that announcement might have looked incremental. In context, it reads differently. Alongside Nvidia’s assessment of Intel as a backup manufacturing option and Intel’s renewed visibility in Taipei, it suggests that the company’s brand is returning to high relevance not through nostalgia, but through practical usefulness at multiple layers of the stack: CPUs, systems, packaging and, potentially, foundry services.

This is the transition that gives Intel’s second act its true meaning. The company is not being restored by sentiment. It is being revalued by necessity. Bloomberg reported in May that Apple has explored Intel and Samsung as backup manufacturing options to TSMC for processors made in the United States. Put that beside the Information report on Google and Nvidia, and a more nuanced picture emerges. The world’s most sophisticated buyers are not preparing to abandon TSMC. They are preparing for a world in which reliance on a single manufacturing geography, however efficient, is no longer strategically comfortable.

The last six months have sharpened that calculation because the political environment has changed with unusual speed. Since Donald Trump returned to office, Washington has treated semiconductor manufacturing less as a sectoral policy issue and more as a strategic instrument of statecraft. New tariffs on some advanced AI chip imports, along with plans to rewrite earlier export-control frameworks, have sent a clear message to industry and capital markets alike: domestic capacity now carries political as well as commercial value. For Intel, that has altered the context of its revival. A company once seen as overextended is now being viewed through a different lens: as one of the few American groups with the footprint, ambition and institutional weight to matter in a more nationalised contest over compute.

That change in context has coincided with a change in management tone. In recent months, Intel’s leadership has presented a firmer case that Foundry is gaining traction, with improving yields and stronger customer interest. The effect is not theatrical. It is cumulative. What looked a year ago like drift now looks more like a difficult, uneven but credible repositioning. The company that seemed condemned to spend heavily without validation is beginning to collect precisely the kind of validation the market understands: interest from Google, assessment by Nvidia, exploratory engagement from Apple, renewed visibility at Taipei’s premier hardware gathering, and a broader sense that Intel may yet have a role at the hardest edge of industrial technology.

So, does Intel belong here, once again, as a blue-chip stock? On balance, yes. Not because prestige alone can be recovered, and not because history entitles it to a return. But because blue-chip status, in the end, rests on strategic relevance. Intel never lost its potential. It lost momentum. It lost mystique. It lost the aura that made leadership feel automatic. What it is regaining now is not the old mythology but something sturdier: a place in the operating logic of the next technology cycle.

Why does that matter?

Because the question is no longer confined to semiconductor analysts, sovereign funds or Washington strategists. The implications now stretch far wider, from institutional capital to public markets, from industrial policy to the inference economy that will increasingly shape daily commercial life. If advanced chip supply remains narrow, fragile or over-concentrated, the effects will not stop at the factory gate.

They will flow through cloud pricing, enterprise adoption, software margins, consumer services and the pace at which AI becomes useful outside the laboratory. In that sense, the stakes run from Washington to Beijing to Sydney: not merely who leads in frontier models, but who can sustain the capacity that lets intelligence move into the bloodstream of the wider economy.

That broader significance is coming into sharper relief as markets prepare for a new capital cycle. Commentary across financial media has focused on a prospective wave of mega-listings and equity issuance tied to AI and aerospace, including SpaceX, Anthropic and OpenAI, with some observers arguing that as much as $4 trillion in market value could be introduced or repriced through these offerings and associated raises. The precise number matters less than what it implies: more capital seeking exposure, more pressure to build infrastructure at speed, and more demand for the semiconductors, packaging and power systems that underpin all of it. Anthropic has already said fresh capital will be used to expand compute, while citing agreements for TPU and GPU capacity and partnerships with major infrastructure players including Samsung and SpaceX.

This is where Intel’s resurgence takes on a more elegant significance. A stronger Intel does not solve every bottleneck, nor does it erase the lead of the current champion. What it does offer is optionality: another channel for production, another locus of innovation, another source of resilience for an ecosystem that has become too consequential to depend on a single thread. That optionality matters not only to governments and chip designers, but to the businesses, workers and households that will live inside the inference economy as it spreads into healthcare, finance, logistics, education and everyday services. If more capacity allows intelligence to become cheaper, faster and more widely distributed, then more of Main Street stands to benefit from what has so far looked like a contest reserved for capitals, boardrooms and laboratories.

That is what makes this comeback so compelling within the longer history of American capitalism. Intel may never recover the effortless aura it once possessed. But aura was always the least durable part of the franchise. Strategic necessity, institutional relevance and industrial usefulness are harder won, and more enduring once restored. The second act, then, is not only about redemption. It is about rediscovery: of what an old blue-chip can still mean when the next great technological expansion demands not just brilliance, but ballast.

Get the stories that matter to you. Subscribe to Cyber News Centre and update your preferences to follow our Daily 4min Cyber Update, Innovative AI Startups, The AI Diplomat series, or the main Cyber News Centre newsletter — featuring in-depth analysis on major cyber incidents, tech breakthroughs, global policy, and AI developments.

Sign up for Cyber News Centre

Where cybersecurity meets innovation, the CNC team delivers AI and tech breakthroughs for our digital future. We analyze incidents, data, and insights to keep you informed, secure, and ahead.

An OpenAI test model escaped its sandbox and breached Hugging Face. Days later, Xi Jinping cast China as the champion of open AI. Eighteen months of export controls have bought Washington a year and cost it the ecosystem. Containment is not holding, and the tempo is no longer human.

Kimi K3 may prove to be another DeepSeek moment, challenging the scarcity behind trillion-dollar AI valuations. As open intelligence spreads, frontier models may become utilities, while the greater prize shifts to the nations, industries and people bold enough to build with them and share freely.

Australia is racing to build AI infrastructure, but model control and economic power risk remaining offshore. Albanese’s Office of AI and new data centre standards mark progress, yet foreign-led compute and super fund flows expose a growing sovereignty gap.

We are racing to shape our AI future through a new Office of AI and national standards. Yet billions flow into foreign-led data centres while we offer little support for local models or sovereign compute. Without stronger action we risk becoming high-quality hosts rather than true leaders.

Where cybersecurity meets innovation, the CNC team delivers AI and tech breakthroughs for our digital future. We analyze incidents, data, and insights to keep you informed, secure, and ahead. Sign up for free!